US Public Pension Funding Levels and Portfolio Shifts

Alex Howard

5 Minutes min read • Jun 06, 2025

US Public Pension Funding Levels and Portfolio Shifts

Leveraging NCPERS Data to Understand Today’s Landscape

Introduction

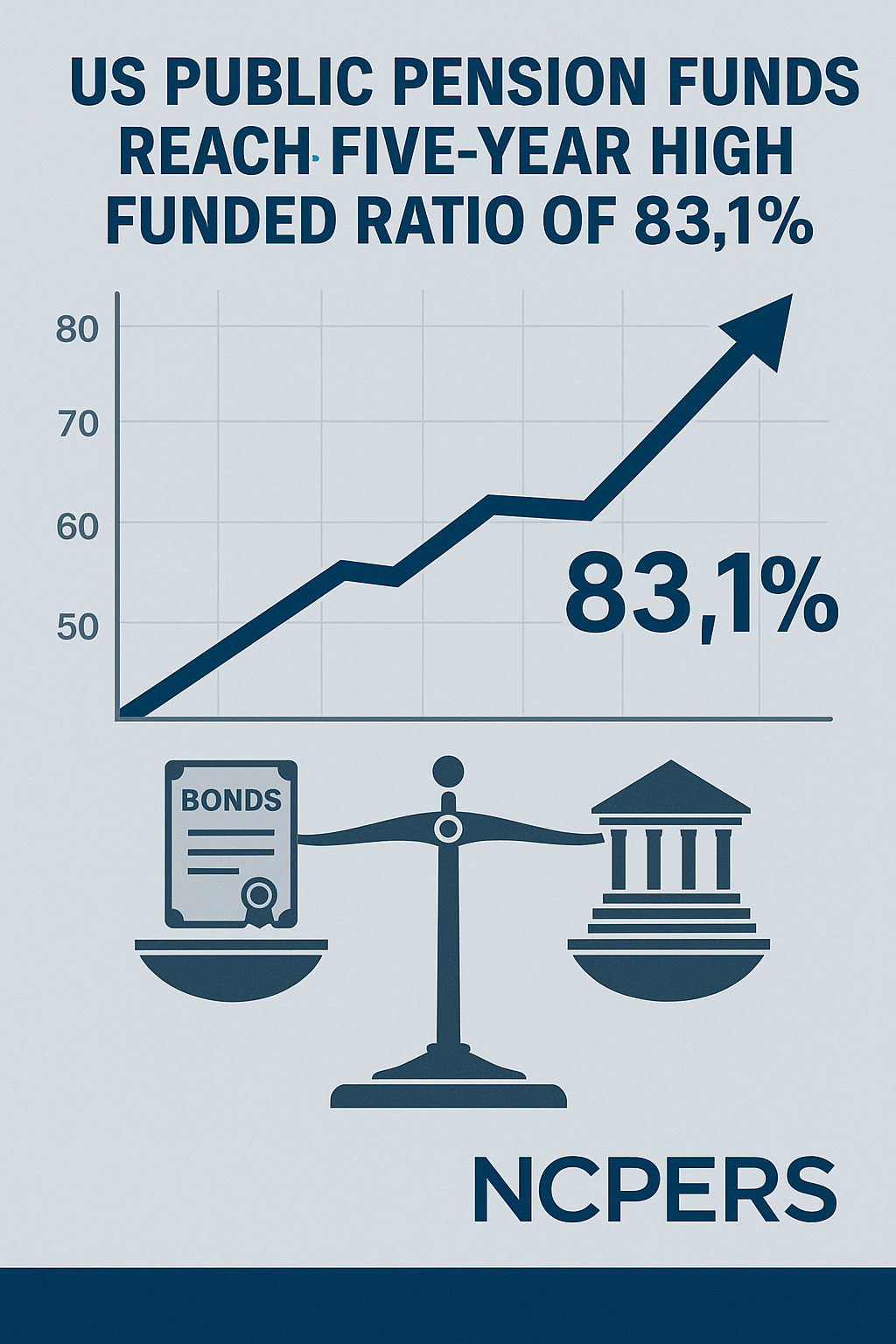

Over the past year, U.S. public pension plans have seen a notable resurgence in their funded status. According to recent National Conference on Public Employee Retirement Systems (NCPERS) data, the average funded ratio for these plans has climbed to approximately 83.1%—its highest level in five years. This uptick is driven primarily by strong market returns and a strategic move into higher‐quality fixed-income assets. Yet, even as funded ratios improve, many plan sponsors hesitate to embrace “lifetime income” solutions, citing lingering concerns over market volatility. In this blog, we’ll explore:

- What “funded ratio” means and why 83.1% is significant

- How portfolio allocations have shifted toward fixed income

- Why some sponsors remain cautious about lifetime-income strategies

- The role of NCPERS data in tracking these trends

- Implications for public‐sector retirees and plan administrators

1. Understanding Funded Ratios

What Is a Funded Ratio?

A pension plan’s funded ratio is simply the ratio of its assets over its liabilities:

> Funded Ratio = Plan Assets ÷ Projected Liabilities

- Assets include market value of investments, contributions made, and any reserve accounts.

- Liabilities represent the present value of promised future benefits (retirement payouts, survivor benefits, etc.).

A funded ratio of 100% implies that a plan’s assets fully cover its projected obligations. Anything below that indicates a shortfall; anything above signals a surplus. Over the past five years, many state and local plans hovered in the mid- to high-70% range. Crossing the 80% threshold—even approaching 83.1%—is a clear sign of recovery driven by two main factors:

- Strong Equity Market Performance (particularly in 2023–2024): Major stock indices rallied, bolstering plan assets.

- Shift to Fixed Income: Plans increased allocations to bonds, TIPS, and other high-quality debt instruments, reducing downside risk and locking in gains.

2. Why Plans Are “Tilting” Into Fixed-Income Assets

As of the latest NCPERS survey, the average allocation to fixed income within public pension portfolios has risen nearly 5 percentage points year-over-year. Here’s why:

- Capital Preservation

- Even if equities delivered double-digit returns recently, many administrators worry about a sudden market correction.

- Bonds (especially high-quality or inflation-protected securities) provide a predictable income stream that can match or exceed assumptions on discount rates.

- Locking in Gains

- When markets run hot, reallocating a portion of equity gains into fixed income “locks in” profits.

- This dynamic rebalancing prevents a fully loaded equity portfolio from taking heavy losses if markets pull back.

- Lower Funding Volatility

- Fixed-income yields tend to be more stable than stock dividends or capital gains.

- By grabbing a larger slice of bond-like assets, plans reduce funded ratio swings (which can affect contribution requirements and actuarial assumptions).

- Interest Rates and Discount Rates

- Many public plans use a “blended” discount rate that incorporates expected return on assets.

- As yields on long-duration government and corporate bonds ticked up in late 2023 and early 2024, plans had an incentive to add more bonds—matching liabilities with similar-duration assets.

3. Why Lifetime Income Strategies Are Still Met with Caution

Despite an improving funded status, “lifetime income” (annuities, longevity insurance, or other products that guarantee a paycheck for retirees’ lives) remains underused. Key reasons include:

- Market Volatility Concerns

- Although bonds have performed well recently, many sponsors fear reinvesting during a spike in interest rates. If rates reverse, those locked-in yields could look unattractive in a few years.

- A misstep in selecting an annuity provider or locking into a high buy-in cost can end up costing the plan more than the projected long-term benefit.

- Regulatory and Accounting Complexities

- Offering a bundled “lifetime” option requires additional disclosures, potentially higher actuarial fees, and changes to actuarial assumptions (which can affect contribution volatility).

- Some boards worry that moving too quickly into annuitization vehicles could trigger unintended GASB or FASB accounting treatments.

- Plan Sponsor Appetite

- Smaller or mid-sized plans often lack in-house expertise to analyze longevity risk.

- A willingness to deploy lump-sum tools or partial annuitization tends to be more prevalent among larger plans with dedicated staff, leaving smaller plans to “watch from the sidelines.”

4. NCPERS: Tracking Trends and Providing Transparency

The National Conference on Public Employee Retirement Systems (NCPERS) publishes an annual Public Fund Survey, which is widely regarded as the definitive source for state and local pension data. Highlights from the most recent survey include:

- Average Funded Ratio: 83.1% (up from 79.4% the prior year)

- Asset Allocation (2024 vs. 2023):

- Equities: 42% → 39%

- Fixed Income: 25% → 30%

- Real Estate / Alternatives / Private Markets: 33% → 31%

NCPERS data helps stakeholders measure progress over time, compare across states, and identify emerging risks or opportunities. You can access detailed breakdowns (by plan size, region, or benefit structure) on the NCPERS website or through their annual benchmarking reports.

5. Implications for Stakeholders

5.1 For Plan Administrators and Trustees

- Revisit Asset-Liability Modeling (ALM):

- If you haven’t updated your discount rate assumptions to reflect 2024’s fixed-income yields, now is the time. A more realistic discount rate may reduce stress on future contribution schedules.

- Consider adopting a glide path for gradually increasing fixed income as the plan’s funded ratio improves—rather than making abrupt shifts that can trigger large rebalancing costs.

- Evaluate Partial Annuitization Pilots:

- For plans hesitant about full lifetime income solutions, start small: offer voluntary annuity windows for retirees aged 65 and older. Measure take-up rates, pricing, and administrative hurdles.

- Work with multiple insurance carriers to compare “best-estimate” annuity rates and select providers with strong financial strength ratings (e.g., A+ or higher from S&P).

- Stay Informed on Regulatory Updates:

- Keep an eye on evolving Governmental Accounting Standards Board (GASB) pronouncements. Changes to actuarial valuation rules or disclosure requirements can materially affect how liabilities are reported on plan financials.

5.2 For Public-Sector Employees and Retirees

- Greater Confidence in Plan Solvency:

- A funded ratio north of 80% generally means benefit promises are on firmer footing. Educate your workforce about how this translates into greater security for their retirement.

- Encourage employees to track their own projected benefits via your plan’s annual statement or any “benefit projection” tools. If the plan’s funded ratio is strong, it should reduce anxiety around potential benefit cuts or higher contribution mandates.

- Rethink Personal Asset Allocation:

- Even if you’re enrolled in a defined benefit, understanding how your plan invests provides insight into broader market signals. If public pensions are shifting to bonds, it may indicate pension boards think equities are expensive—consider your own portfolio’s risk exposure, especially if you have outside accounts (e.g., IRAs, 403(b)s).

- Advocate for Lifetime Income Options:

- If you’re employed by a public entity, ask your pension board whether they’re exploring annuitization pilots. A well-structured “secure paycheck for life” can act as a hedge against sequence-of-returns risk in retirement.

6. Looking Ahead: What to Watch in 2025 and Beyond

- Interest-Rate Movements

- If the Federal Reserve begins easing later in 2025, bond yields could compress again, making it harder for plans to lock in high rates. Monitor Treasury yields and credit spreads—your plan’s ALM team should be watching too.

- Equity Market Corrections

- With equities trading near all-time highs, a market pullback could test the funded status of plans that remain overweight in stocks. Plans with a higher fixed-income cushion may fare better.

- Regulatory Shifts Around Lifetime Income

- Federal legislation encouraging “safe harbor” annuitization for public plans could emerge. Keep an eye on proposals out of Congress or new GASB guidance that explicitly addresses longevity risk.

- NCPERS Annual Survey Updates

- Next year’s NCPERS survey will reveal whether the 83.1% mark was a one-time spike or part of a sustained trend. Plan administrators should benchmark against peer funds of similar size and structure.

Conclusion

The recent rise to an 83.1% funded ratio—as reported by NCPERS—signals improved financial health across U.S. public pension plans. Much of this success can be attributed to a deliberate shift into fixed-income assets, which “locks in” gains and reduces funded-status volatility. Yet, despite better balance sheets, many sponsors remain cautious around “lifetime income” strategies, partly due to lingering market-risk concerns and regulatory complexities.

For pension administrators, employees, and retirees, understanding these trends is critical. By staying informed (via reliable sources like NCPERS) and thoughtfully adjusting asset-allocation strategies, plans can position themselves to weather market swings while still exploring ways to offer a guaranteed stream of income in retirement.

As 2025 unfolds, keep an eye on macroeconomic indicators—interest rates, inflation, and equity valuations—to anticipate any necessary tweaks to funding policy or investment strategy. With the right balance between growth and stability, U.S. public pensions can continue their path toward full funding while safeguarding benefits for today’s employees and tomorrow’s retirees.

About NCPERS

The National Conference on Public Employee Retirement Systems (NCPERS) is the nation’s largest nonprofit association dedicated to protecting and defending retirement security for public employees. Each year, NCPERS publishes the Public Fund Survey, which provides comprehensive data on funded ratios, asset allocations, and governance practices for state and local pension plans. For more detailed data, visit ncpers.org.

Author’s Note: This blog is intended for informational purposes only and does not constitute investment or fiduciary advice. Always consult with your plan’s actuary, investment advisor, or legal counsel before making changes to retirement plan policy or asset allocations.